We're getting near an interesting crossroad.

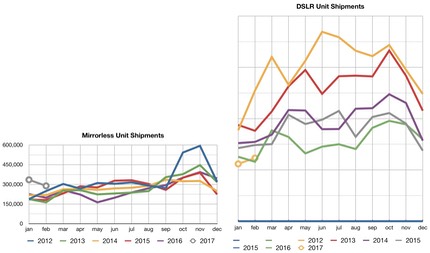

In the ILC market, mirrorless as a percentage of all ILC cameras has slowly been climbing. For 2013 through 2016 the numbers go 19.3%, 23.8%, 25.6%, 27.2%. I'll bet that mirrorless will cross the 30% threshold this year (2017; for the first two months of 2017 we're at 37%, but that probably won't hold).

Some of that crossover is inevitable. The DSLR duopoly of Canon/Nikon has something like 20 total DSLR products on the market—a bit more if you count some of the previous generations still hanging out in inventory—but the mirrorless world is generating 20 new cameras a year. The likelihood that Canon and Nikon introduce super interesting new DSLRs in any given year is less than the likelihood of a super interesting new mirrorless product being announced. So the basic marketing message is stacked against DSLRs.

But frankly, what more would you want from a DSLR that Canon and Nikon haven't already provided? DSLRs are extremely mature products with very high quality and performance capabilities coupled with near exhaustive feature sets. Sure, we'll see iterations of these products that push them faster, with more pixels, and with even more features. But the real question is how many people would actually find those things useful?

Selling a DSLR today is a marketing problem. I'll give you an example from a different market: I have a very capable 10-year old vehicle that's got fairly low mileage on it and is in excellent shape. It suffices for all the things I need a vehicle for. Why would I want a new one? Well, the auto maker's marketing would have to somehow convince me that there's something missing in my current vehicle that I actually need or would find useful.

Not that those things don't exist. It would be nice to have AirPlay in my vehicle—though I can add that through third-party electronics—and it would be nice to have some of the newest safety changes, particularly the auto braking, lane change warning, blind spot warning, and better back-up systems in the latest vehicles. I'd love to have a hybrid vehicle, too. But have those things risen to a high enough level to get me to abandon a perfectly fine vehicle and pay lots of money for a new one?

That's the DSLR problem in a nutshell. Do I need something better than a D810? Probably not, though I sometimes use a Sony A7rII to have a smaller-than-Nikon-DSLR kit (and as I've noted, it's really the competent and reasonable-sized f/4 zoom set that makes for most of the "smaller" bit), and I'm intrigued-but-not-convinced by the medium format cameras that are appearing.

Mirrorless does add some things that DSLRs are a bit behind the times on. The use of an EVF, for example, provides a more what-you-see-is-what-you-get view of the world on most mirrorless cameras, we also get real-time focus peaking info and exposure histograms, too. All three of those things can be very useful to someone that isn't using their cameras all the time, as they're helpful feedback mechanisms that are faster than "shoot the image, review the image, change the settings, repeat until correct."

But the real issue for Canon and Nikon is this: ultimately it's cheaper to make a mirrorless camera than a DSLR of equal capability. There's no doubt in my mind that both companies will push harder into mirrorless sometime soon. Indeed, the EOS M5/M6 appears to be the first of Canon's truly serious attempt to get a mirrorless product right. Nikon can't be too far behind, though let's hope that we don't see EOS M and M3 type experiments first.

I used the word "crossroad" above and I mean it. It won't happen this year or probably not even next, but I'd guess that mirrorless will have a greater volume than DSLR by 2019 or 2020, somewhere in that range. The exact timeframe will depend upon when Canon and Nikon really ramp seriously in mirrorless and how fast they bring their mirrorless offerings up to DSLR-levels of performance and features.

Don't get me wrong. DSLRs won't go away, particularly at the high end (basically 77D and up for Canon, D7200 and up for Nikon, and especially full frame). Anything you can do in a mirrorless camera you can add to a DSLR, so the claims that mirrorless will someday do things that DSLRs can't is, I think, mostly incorrect. To some degree, Sony's SLTs have already proven that. I'm thinking more along the lines of "hybrid," where the viewfinder itself can flip between optical and EVF. I wouldn't be surprised if the 1DxIII and D6 we get for the 2020 Tokyo Olympics are just that: have it both ways.

So the crossroad is this: ILC slowly becomes mirrorless as mainstream, DSLR as smaller high-end niche.

But the road ahead is narrower.

ILC volume shows no real sign of stabilizing: the numbers go 20m, 17m, 13.8m, 13m, 11.6m. They might hold at around the 11m mark this year partly because of all the delayed entries we didn't get in 2016 due to the sensor shortage. I'd also tend to characterize a fair amount of the volume we're getting now as simple customer iteration coupled with sampling. The customer iteration cycle—the time between when they update a current camera to a new one—is growing; currently somewhere above two camera generations and getting larger. The current customer sampling is a bit higher than it will eventually be as things eventually settle down and people pick their horses for the next race. I would not be surprised to find that at the point where we finally hit the crossroad, the overall ILC volume has dropped to 9m units a year.

At current market shares, that means:

- Canon — 4.5m units a year (currently somewhere around 5.5m)

- Nikon — 2.4m units a year (currently somewhere around 3m)

- Sony — 1.3m units a year (currently somewhere around 1.6m)

- Everyone else — 800k units a year (Olympus alone claims currently at 400-500k)

Given the market dynamics I mention—switch of mirrorless/DSLR dominance, smaller market—Canon's switch to automated manufacturing and now seemingly competent mirrorless camera offerings means they'll be aggressive at keeping that 50% market share. They have the cost factors already in place to do so, they now only need to show that they know how to expand their mirrorless line correctly and usefully, while protecting themselves in the declining DSLR market.

- What Canon needs: more models, more lenses

Sony seems to have taken a slightly different approach in the past few years, moving further upscale and less worried about volume. Thus, their market share hasn't really budged much from where they started in ILC, though their profitability certainly has risen. Moreover, Sony still cameras share the E/FE mount with Sony video cameras (as well as some sensors), so they're getting bigger returns for their R&D bucks. Smart move, overall, though they really would like to get a larger piece of the market.

- What Sony needs: a model that really breaks through and increases market share (I'd argue that is likely to be APS-C, and to do so they'll need more and better E-mount lenses, and they need to keep the price from creeping up too much)

The remainder (less Nikon, which I'll get to last) of the players are in a very tight squeeze. While m4/3 pioneered mirrorless and was the first to build full systems of cameras and lenses, the m4/3 market share has been in decline. Olympus just can't seem to budge above 500k units/year, and the financial/organizational situation there probably has them now entrenched at or near that level. Panasonic just moved the consumer camera group to the Appliances division in an apparent though unspecified as of yet cost-cutting move, which seems to indicate that they, too, are in a financial/organizational situation that's not going to net them growth.

Fujifilm is growing, but they started late and from zero; their growth has some turbulence they're likely to hit soon. Still, of the mirrorless players, they're clearly the one making good decisions that are leading to increased sales. Because of that, they're dangerous. They could break out from the single-digit market share to double-digits, and that will mostly come at the expense of Canon, Nikon, and/or Sony.

- What the other players need: a growing market instead of a shrinking one

Finally, we get to the wild card in ILC, and that's Nikon. Nikon is the canary in the coal mine. They're a company that was part of a strong camera duopoly (or triopoly if we include compact cameras) that is totally exposed to the market as a company. More than half their revenues come from cameras (it peaked near 75% of their revenues, currently around 60%), and virtually all of their profit for a number of years now has come from cameras. If Nikon trips up on cameras, Nikon is at high risk of total business failure.

I'd argue, however, that even if Nikon trips up on cameras, that really doesn't present a lot of long-term benefit to the other players, nor does it really change the dynamics of the industry. It would take a bit of pressure of the declining market off the other players, sure. But consider this: If Nikon were to go "poof" today and disappear completely, just redistributing their market share would mean we would have Canon at 63%, Sony at 18%, the rest with 9%. So all that happens in that disaster scenario is that the duopoly becomes Canon/Sony instead of Canon/Nikon, and that Canon becomes more of the strong-arm.

So critical to the coming crossroads is one thing, and one thing only: what Nikon does in mirrorless. If they botch that, Nikon will shrink as a player and end up, best case, as a far smaller player making just niche DSLRs that continue to appeal only to all those owning those 100m Nikkor lenses in the wild. Worst case, they get absorbed by someone else, as Pentax was in the late film, early DSLR era.

- So what does Nikon need? A mirrorless hit, basically. It needs to be priced right (<US$1000), it needs to be spec'd right, it needs to have high quality and performance parameters, and it needs—do I hear a buzz?—a real lens set. I'd argue that it needs more than all that, too. It needs to be a camera that can tie in to social networking easily. Easier than SnapBridge ;~).

Meanwhile, Nikon has another problem: what to do about the mirrorless customers they already have. That's not a small group, though it's not a particularly active buying group these days. Still, the J5 and V3 haven't been iterated in two years, no new lenses have appeared, and Nikon has been totally silent in marketing, too, leaving the two-year old marketing messages pretty much alone while the market changes around them.

If Nikon just says bye bye to the Nikon 1, this gets added to them saying bye bye to the DL models, and who knows what else (cough: KeyMission)? Which means that people aren't going to be terribly interested in what Nikon comes up with next outside of DSLRs because it has a higher likelihood of being abandoned.

All that said, Nikon is still the one to watch. The DSLR era got kicked off by Nikon in a big surprise to everyone else with the D1, and that came at the end of period where Nikon's market share was slipping significantly and they were perceived as being "behind." I have no doubt that Nikon has technological prowess to pull off another surprise. The question is do they have the courage to take that risk again?

But if Nikon doesn't come back into the mirrorless market with guns blazing, just who is going to set the ILC world on fire again? Canon's taking the iterative, protective approach. Olympus/Panasonic made an early impact to get things kicked off, but have lost traction, despite some engineering marvels. Medium format is just too expensive to resurrect ILC cameras, and to a lessor degree, so is Sony FE.

So say what you want about Nikon. We should all want them to succeed in the way they succeeded at the end of the film era: with a surprise that kicks off a new period of growth. Or at least manages to halt the decline.