(news & commentary)

In Olympus’ fiscal year-end report, the headline on the Imaging Division overall presentation was, in Olympus’ own words: "Large degree of failure to meet target for mirrorless camera net sales.” Specifically, Olympus called out dropping prices on Pen cameras, but there’s much more going on in their underlying numbers than just that.

The bottom line was a 13.9b yen loss for the division, previously forecast to be only about 60% of that number. They missed their target mirrorless sales by 5b yen in the first quarter of 2015 alone. They were actually closer to their target in the quarter with their compact camera sales, though those also didn’t meet expectations.

Yet, despite the on-going problems, Olympus has posted their usual forecast: breakeven in the coming year. That same forecast suggests this: that sales will go down 13.8b yen in the coming year, but operating income will increase by the same amount so that everything is essentially a wash. Good luck with that. Why? Because SG&A expenses hit an astounding 62.6% of sales for the year. All those instant rebates, refurbished product, sales, and other discounts are just eating away at the division.

Let me put that in some form of perspective. If I create a tech product like a camera, I’ll generally target a cost of parts, manufacturing, and packaging of perhaps 50% of the price I receive for it. In other words, a gross product margin (GPM) of 50%. Most tech companies have real GPMs in the 35-45% range. When my sales, general, and administrative expenses (SG&A) exceed my GPM, there’s no chance of making a profit. I’m essentially giving away money by producing a product in that situation.

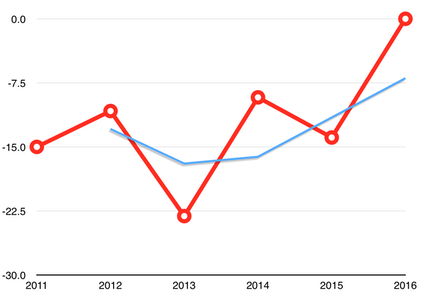

Here’s the rub on what Olympus announced to shareholders: they’re going to reduce sales in Imaging from 83.8b yen to 70b yen in the coming year. Somehow, they’re also going to reduce their loss from 13.9b yen to 0 at the same time. So, let’s assume that they have a GPM of 40%. The cost to produce 70b of product is 42b yen. That leaves them 28b yen for SG&A, best case (assumes no other costs, such as write-downs, inventory build-up, etc.). That means that SG&A for the coming year needs to be 60% lower than last year in order to breakeven. That would be miraculous efficiency for a company that hasn’t produced anything close to that in the last several years (chart below shows last five years of negative results plus next year’s estimate in red, the blue line is the moving average):

Meanwhile, in terms of unit volume, the mirrorless unit sales have gone like this:

- Fiscal 2014: 510k units

- Fiscal 2015: 510k units

- Fiscal 2016 forecast: 480k units

In other words, no growth in terms of unit volume for mirrorless, though there may be a shift towards higher priced cameras long term.

Olympus has been repeating the same chant for years now: "yes, we did poorly, but we’ll hit breakeven soon, maybe even next year.” This year is no different. They did poorly, they expect to manage break even during the year. The problem is that there’s nothing in the actual financial information they’ve posted that would give that any credibility. To produce a better bottom line while sales are contracting so much, you’d have to be beyond ruthless about cutting costs, reducing staff, jettisoning facilities, getting SG&A down to where it should be, and so on. There’s really nothing in Olympus’ statements that indicate that they are doing those things (and many of those things would incur a write-down if made, reducing income and generating another loss ;~).

I’m going to repeat: I really would love to see Olympus succeed with mirrorless. There’s nothing yet visible to suggest that they’re going to stop trying, only a repeated high degree of over-optimism about their future. So the bottom line is still that the main medical business is subsidizing the imaging business at Olympus, as it has for all of this decade. More and more the Imaging group is becoming a hobby at Olympus, not an actual business with true return on investment.

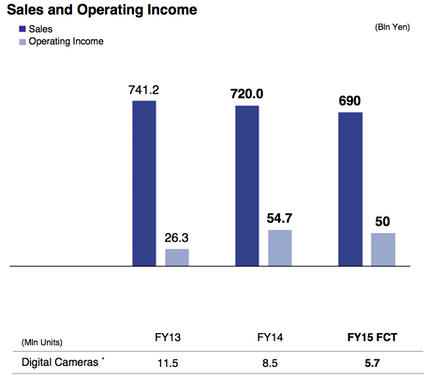

Sony also reported results this week, with this being the key slide camera users are interested in:

Bottom line: fast declining unit volume, slow declining sales, now with flat operating income-to-sales ratios. Sony took a huge restructuring loss in the first quarter of this calendar year, apparently to properly downsize the business. That loss reduced the full year operating income of the group to the number shown above.

Sony also broke out the two primary components of the Imaging group, which is effectively consumer cameras and camcorders versus professional/broadcast gear. As I’ve long expected, the professional side produces more profit per sales dollar than does the consumer side. So be a little careful at interpreting group good news as ILC camera good news.